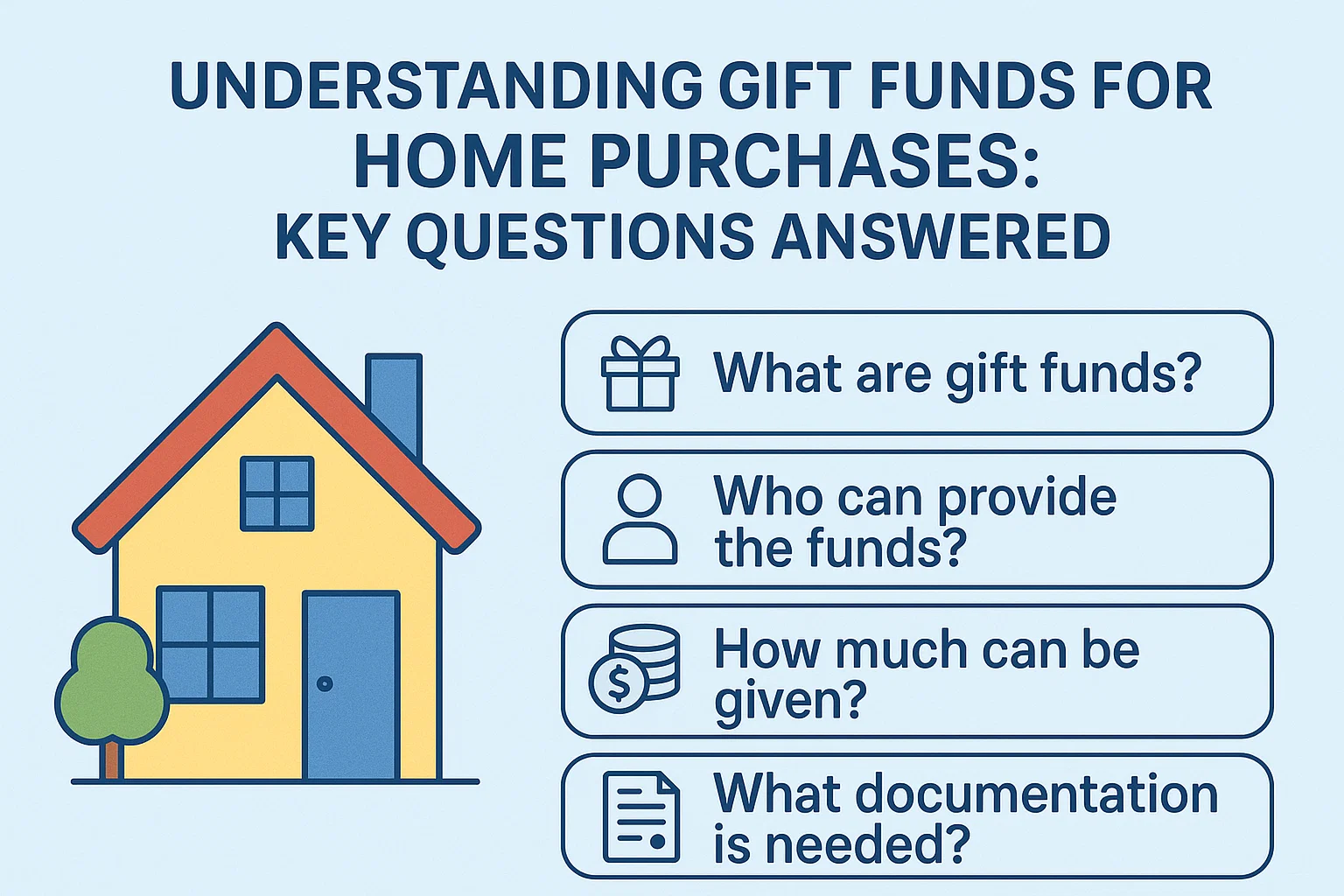

Understanding Gift Funds for Home Purchases: Key Questions Answered

Understanding Gift Funds for Home Purchases: Key Questions Answered

What Types of Loans Allow Gift Funds?

Gift funds can typically be used for down payments or closing costs when purchasing a single-family primary residence. These funds are accepted under most conventional loan programs, provided they meet specific lender requirements.

Who Can Provide Gift Funds?

Acceptable sources of gift funds include:

- Family members, including spouses or fiancés

- Close friends (less common)

- Employers, charitable organizations, or public entities (subject to lender approval)

Donors must provide proof that the gift comes from their own funds, often through bank statements or a signed gift letter.

Who Cannot Provide Gift Funds?

Prohibited sources include anyone with a financial interest in the transaction, such as:

- Home sellers or builders

- Real estate agents or mortgage lenders

- Developers

Funds from these parties are treated as sales concessions or discounts rather than gifts.

What Is a Gift Letter?

A gift letter confirms that funds are a non-repayable gift. Requirements vary by lender, but common elements include:

- Donor and recipient names/contact information

- Gift amount and property address

- Statement confirming no repayment expectation

Some lenders may waive the letter if funds have been in your account for 60+ days (“seasoned”) or if the amount is relatively small.

Additional Considerations

Gifts may have tax implications for both the donor and recipient. Consult a financial advisor or tax professional to ensure compliance with regulations.

Need Mortgage Guidance?

Contact a licensed loan officer to discuss your specific situation and loan requirements.