Homeowners Insurance: Smart Strategies to Lower Costs Without Sacrificing Coverage

Homeowners Insurance: Smart Strategies to Lower Costs Without Sacrificing Coverage

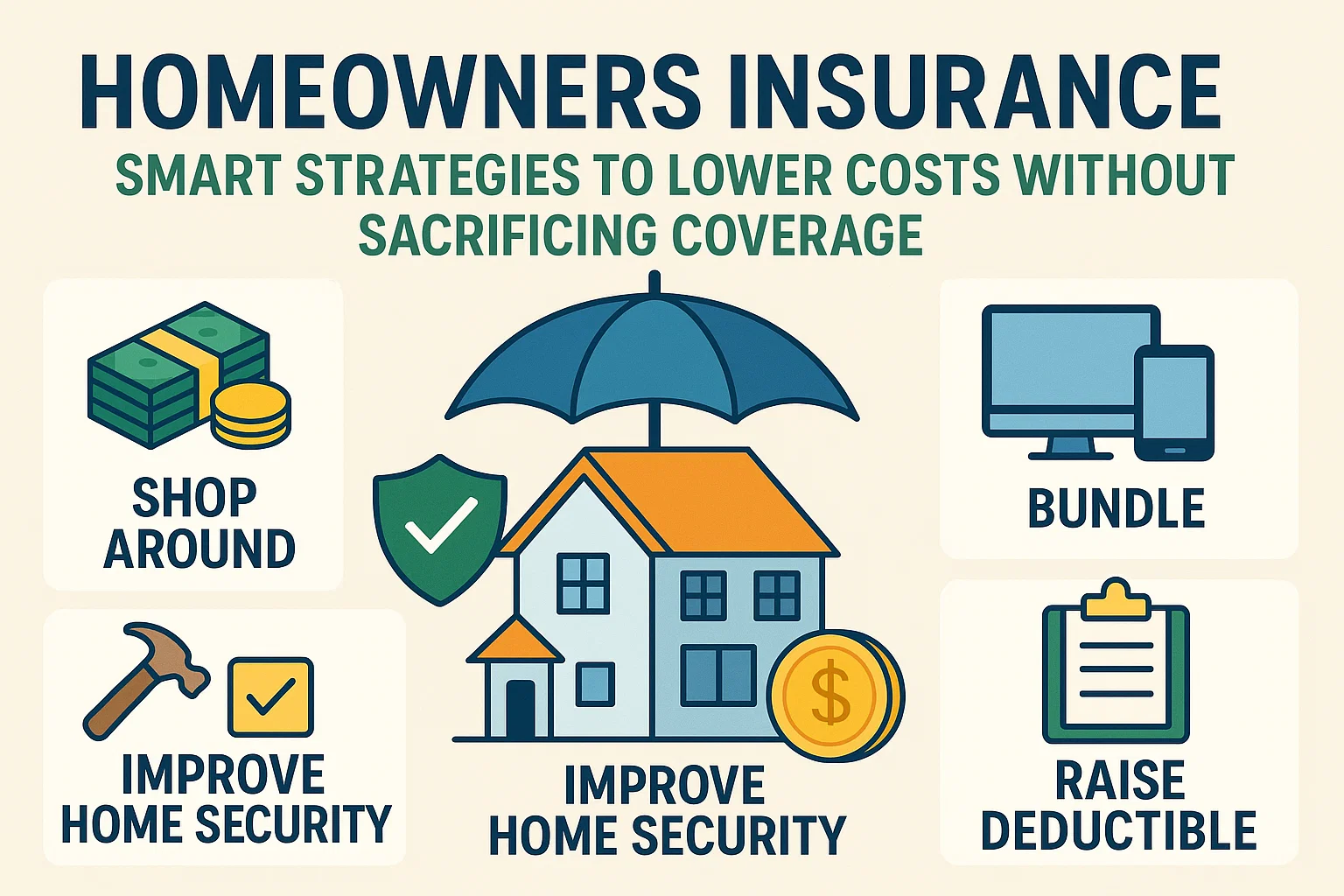

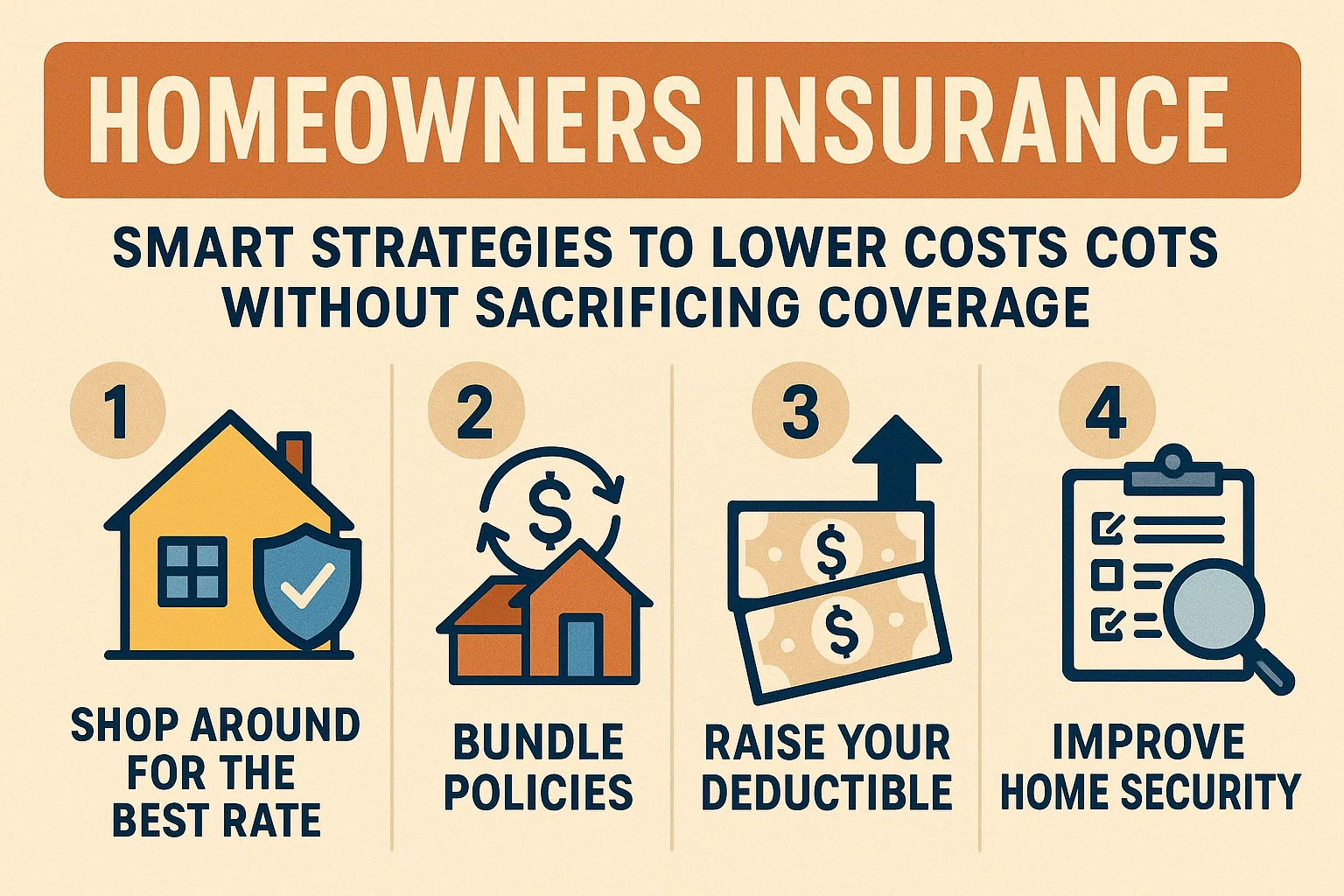

Homeowners insurance is based on replacement cost, so it’s dangerous to try to save a few bucks by cutting back on coverage. Instead, use these proven strategies to reduce premiums while maintaining robust protection:

Shop Around

Premiums can vary dramatically between insurers. A study by Consumer’s Checkbook found price differences of up to $300 for identical coverage. Compare quotes annually to ensure you’re getting the best deal.

How’s Your Credit?

Insurers now use credit-based insurance scores to set rates. Maintain strong credit by paying bills on time and keeping debt levels low to qualify for better premiums.

Claims

File claims only for significant losses you can’t afford out-of-pocket. Multiple small claims—even legitimate ones—can lead to higher premiums or non-renewal.

Deductibles

- Increasing deductibles lowers premiums. Raising from $250 to $500 may save 10% annually; $1,000 could save 20%.

- Never set deductibles higher than what you can comfortably pay in an emergency.

Discounts

- Safety devices: Save 2-15% with smoke alarms, deadbolts, or monitored security systems.

- Loyalty & bundling: Discounts often apply for long-term policyholders or bundling home/auto insurance.

- Special groups: Savings may be available through employers, clubs, or associations.

- Risk reduction: Non-smokers, seniors, and homes near first responders often qualify for lower rates.

Riders

Review specialty coverage for high-value items (jewelry, art, electronics) annually. Cancel unnecessary riders for outdated or depreciated items.

Inventory

Create a detailed home inventory with photos/videos and room-by-room documentation. This simplifies claims and helps verify adequate coverage levels.

Dogs

Certain breeds (pit bulls, German shepherds, Dobermans) may trigger coverage denials or higher premiums. Disclose pet ownership upfront to avoid surprises.

Land

Insure only the structure—not the land. If your property is valued at $300,000 with a $50,000 lot value, insure the home for $250,000.

Final Warning

Price isn’t everything. Prioritize insurers with:

- Strong financial ratings (check A.M. Best or Standard & Poor’s)

- Responsive customer service

- Fair claims handling

- Stable policyholder relationships

Consult consumer guides and ask for personal recommendations to find reliable providers.