Understanding Escrow Shortages: What Homeowners Need to Know

Understanding Escrow Shortages: What Homeowners Need to Know

Receiving an unexpected email or letter from your mortgage company can trigger a moment of panic. However, if you’ve had a mortgage for over a year, you’re likely familiar with annual escrow analyses from your lender. While these notices may not be alarming, understanding them is critical.

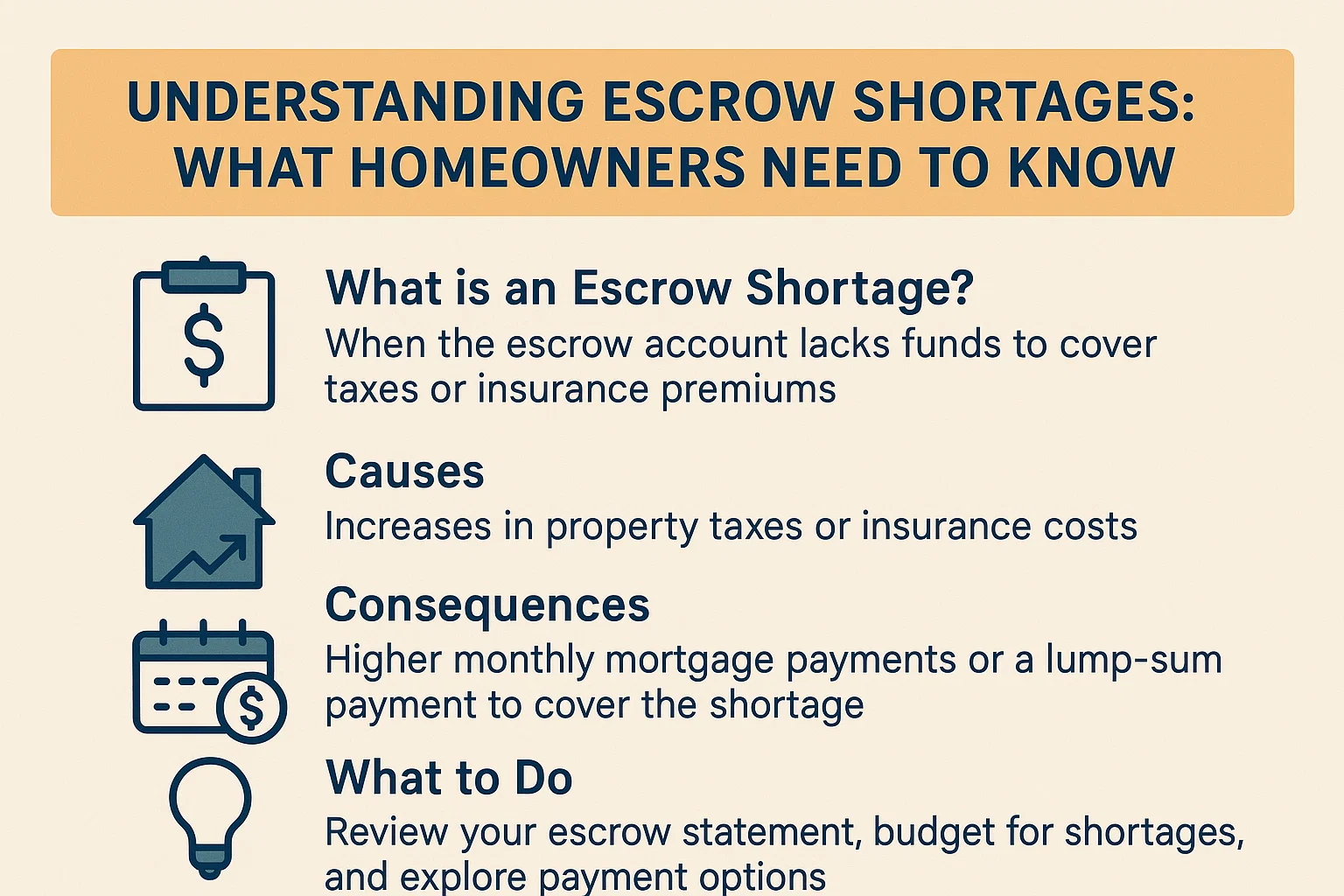

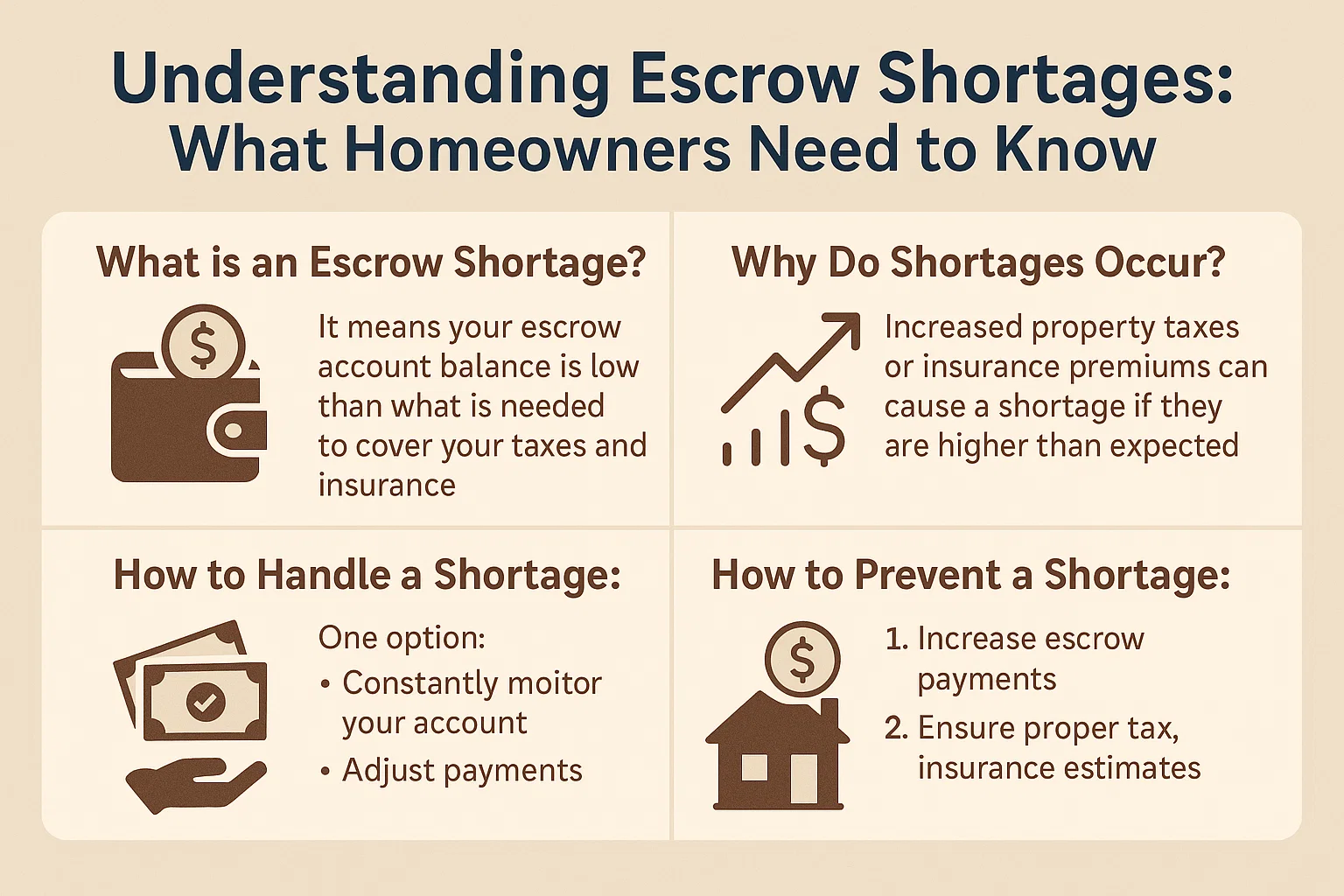

What Is an Escrow Account?

Escrow accounts are managed by mortgage servicers to hold funds for property taxes and homeowner’s insurance. These accounts consolidate bills into one monthly mortgage payment, ensuring timely payments. “The amount paid toward principal and interest on a fixed-rate mortgage doesn’t change—what fluctuates are taxes and insurance costs,” explains a mortgage industry executive.

How Escrow Analysis Works

Mortgage companies conduct an annual review using updated tax and insurance data. “You’ll receive a notification detailing anticipated payouts and adjusted monthly payments to cover future bills,” says a home lending expert. Lenders often collect slightly more than estimated to avoid shortages.

What Causes an Escrow Shortage?

An escrow shortage occurs when collected funds fall short of actual tax or insurance bills. Common causes include:

- Rising home values leading to higher property taxes.

- Increased insurance premiums due to policy changes or risk factors.

Example Scenario

If annual property taxes are $2,400 and insurance is $1,200, your monthly escrow payment should be $300 (plus a cushion). Payments below this amount create a shortage when bills come due.

Addressing an Escrow Shortage

If a shortage is identified, lenders typically offer two solutions:

- Pay the shortage in full: Resolves the issue immediately but requires upfront funds.

- Spread payments over 12 months: Increases monthly payments but eases budget strain.

“Choose the option that aligns with your financial situation,” advises a mortgage professional.

Preparing for Future Shortages

To mitigate surprises:

- Monitor property tax and insurance updates independently.

- Budget for potential payment increases, even with a fixed-rate mortgage.

Final Tips

Review escrow analyses promptly and contact your mortgage servicer with questions. Proactive planning ensures smoother financial management and avoids unexpected hurdles.