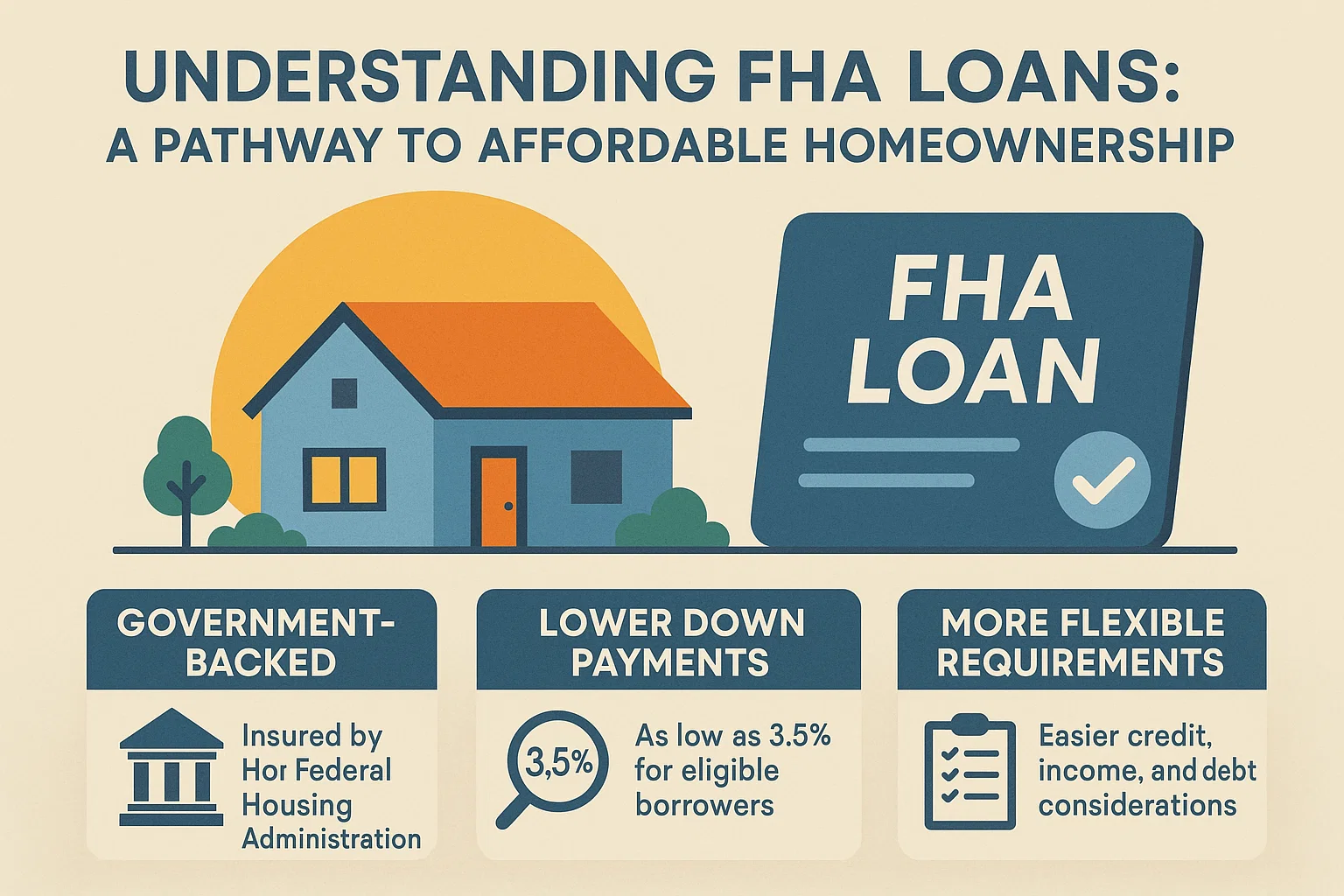

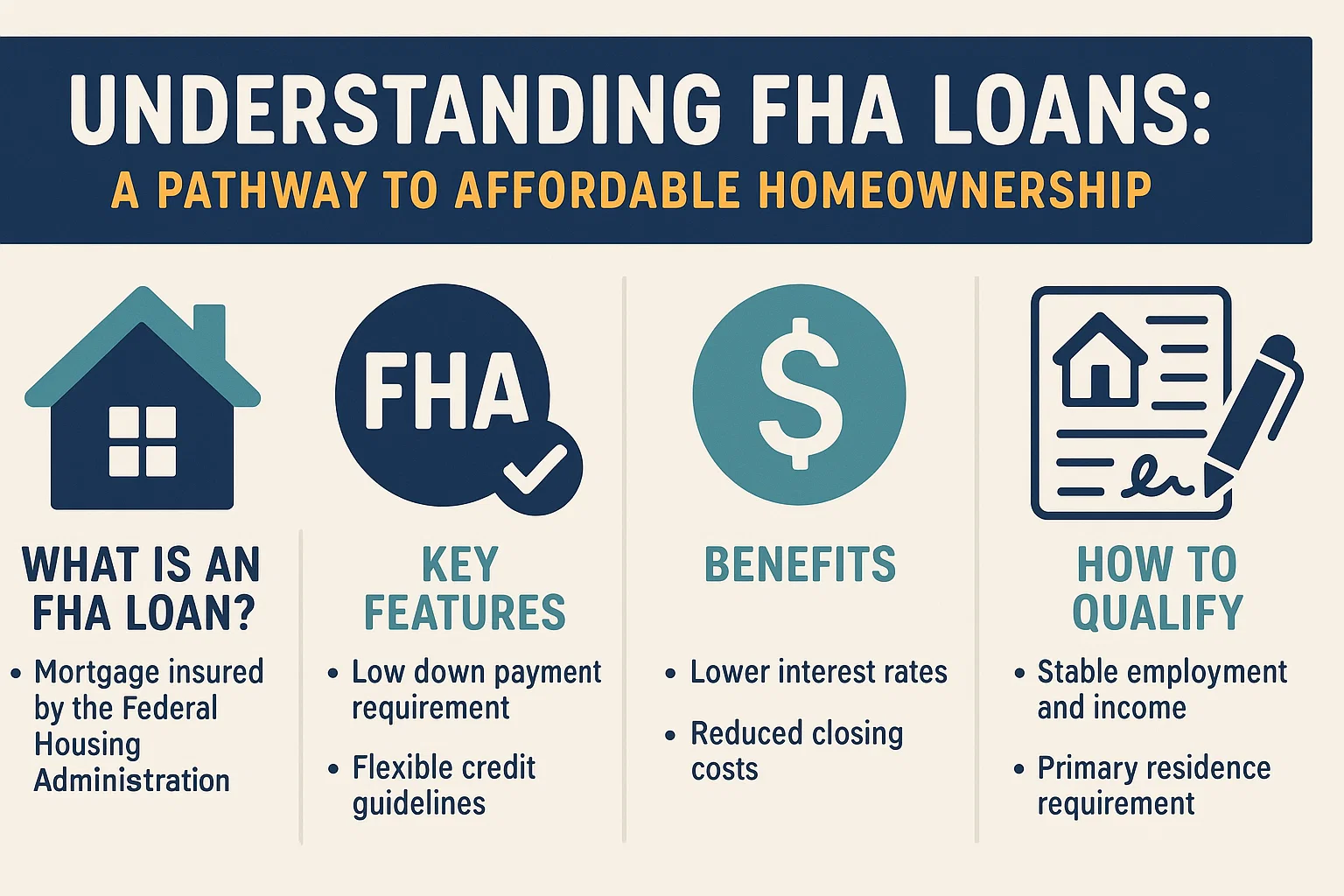

Understanding FHA Loans: A Pathway to Affordable Homeownership

Unlocking Homeownership with FHA Loans

For many aspiring homeowners, the journey to buying a house can feel daunting. Between saving for a down payment and navigating credit requirements, traditional mortgages may seem out of reach. However, FHA loans offer a flexible and accessible alternative, opening doors for buyers who need a little extra support.

What Is an FHA Loan?

An FHA loan is a government-backed mortgage insured by the Federal Housing Administration (FHA). This insurance reduces risk for lenders, allowing them to approve borrowers who might not qualify for conventional loans. If a borrower defaults, the FHA compensates the lender, making these loans a safer option for financial institutions and a lifeline for buyers.

Key Benefits of FHA Loans

- Lower Down Payments: Borrowers can qualify with as little as 3.5% down.

- Flexible Credit Requirements: A FICO score of 580–640 is typically sufficient.

- Debt-to-Income Flexibility: Higher debt ratios may be accepted compared to conventional loans.

- Refinancing Opportunities: Existing homeowners can refinance to secure better rates.

Qualification Criteria

To secure an FHA loan, applicants must meet the following requirements:

- Verifiable and steady income

- Ability to cover monthly housing payments and existing debts

- Minimum 3.5% down payment

- Established credit history

- Property purchase within FHA loan limits

Types of FHA Loans

The most common option is the 203(b) Basic Home Mortgage Loan, designed for purchasing or refinancing a primary residence. Other specialized FHA loans cater to renovation projects (203(k) loans) or energy-efficient upgrades.

Recent Updates to FHA Loans

Recent changes have made FHA loans even more accessible:

- Lower Mortgage Insurance Premiums: Reduced fees ease long-term costs for borrowers.

- Higher Loan Limits: Adjusted thresholds accommodate rising home prices in many regions.

Is an FHA Loan Right for You?

FHA loans are ideal for first-time buyers, those with limited savings, or applicants with imperfect credit. However, consulting with a mortgage specialist is crucial to evaluate your financial situation and explore all available options.