Understanding the 3-2-1 Buydown Mortgage: A Guide to Lower Initial Payments

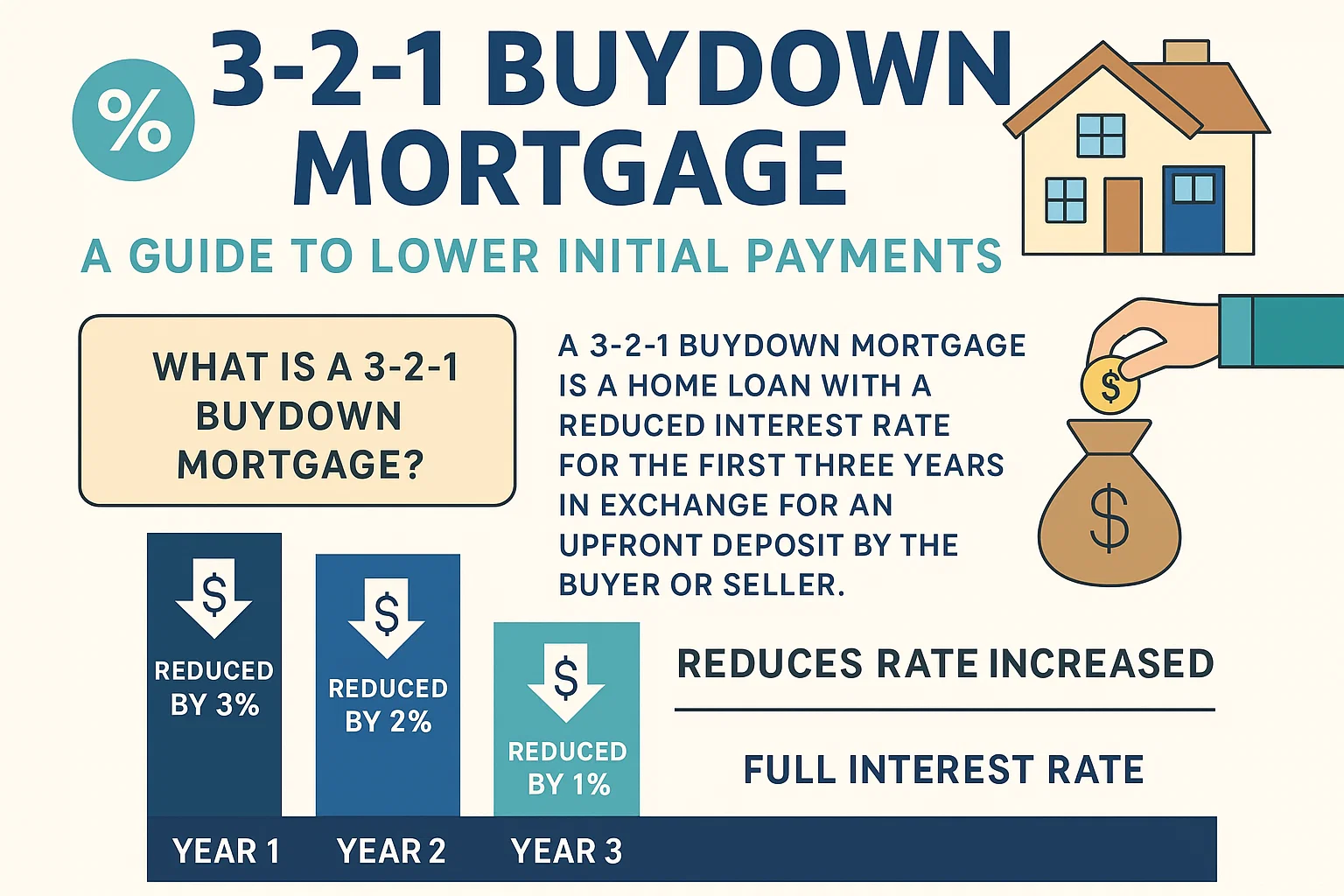

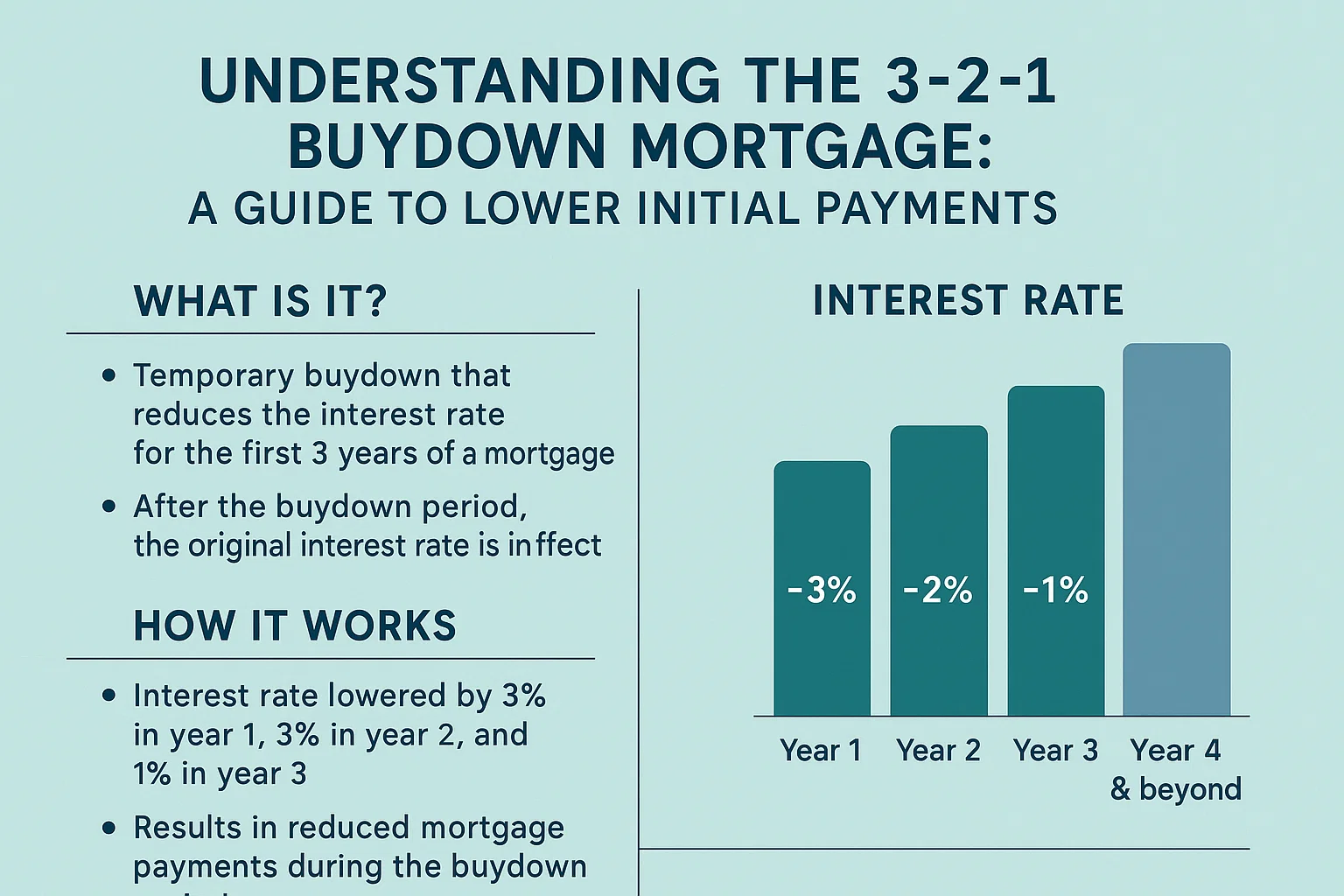

What Is a 3-2-1 Buydown Mortgage?

A 3-2-1 Buydown Mortgage is a financing strategy designed to reduce monthly payments during the initial years of homeownership. This approach helps buyers manage expenses as they transition into their new home, offering a gradual path to full mortgage payments.

How Does a 3-2-1 Buydown Work?

With this buydown structure, the seller or builder covers upfront costs to temporarily lower your interest rate for the first three years:

- Year 1: Interest rate reduced by 3%

- Year 2: Interest rate reduced by 2%

- Year 3: Interest rate reduced by 1%

Starting in Year 4, you’ll pay the full interest rate for the remainder of the loan term.

Example of Savings with a 3-2-1 Buydown

Consider a $300,000 home with a 7% base interest rate:

| Year | Monthly Payment | Rate Reduction | Annual Savings |

|---|---|---|---|

| 1 | $1,407 | 3.875% APR | ~$5,070 |

| 2 | $1,541 | 4.875% APR | ~$3,469 |

| 3 | $1,682 | 5.875% APR | ~$1,776 |

| 4-30 | $1,830 | 6.875% APR | Full payment begins |

Total estimated savings: Over $10,300 in the first three years.

Benefits of a 3-2-1 Buydown

- Lower initial payments to offset moving/furnishing costs

- Tax-deductible buydown costs (consult a tax advisor)

- Flexibility to adjust to long-term payments gradually

Other Buydown Options

Some sellers may offer alternatives:

- 2-1 Buydown: Reduced rates for the first two years

- Permanent Buydown: Lower fixed rate for the entire loan term

Is a Buydown Right for You?

A 3-2-1 buydown is ideal if you expect income growth over time or want to ease into homeownership costs. Always consult a financial advisor or mortgage specialist to evaluate your specific situation.